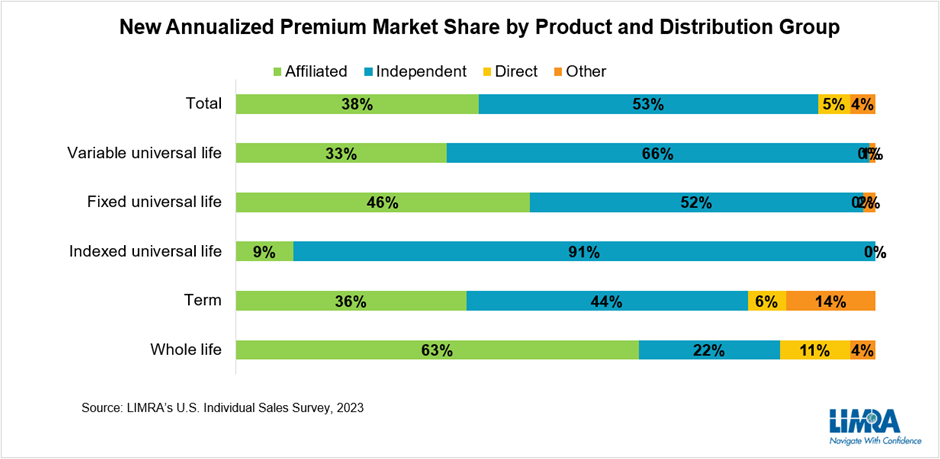

In 2023, independent distribution market share made up 53% percent of all U.S. life insurance new premium sold, compared to just 38% from affiliated agents.

As an example, indexed universal life (UL) new premium, which was negligible in 2011, now represents a quarter of new premium sold today. Independent distribution sells more than 90% of IUL premium. Independent channels also sell a majority of fixed UL and variable UL premium. Even for whole life premium — which remains predominantly sold by affiliated agents — market share for independent channels has jumped nine points in the past decade.

In light of these sales trends, it is clear that all life insurers have to develop multi-channel strategies to remain competitive. Part of that strategy involves building strong relationships with intermediaries, which represent thousands of independent agents.

The Role Of The Intermediary

Intermediaries — primarily independent market organizations (IMOs) and brokerage general agencies (BGAs) — play an essential role with independent financial professionals by helping them build and grow their practices, acting as the expert go-between for financial professionals and carriers. Among the services they offer to agents include training and development, marketing and technology support, underwriting support and case management, and a product platform — vetting products and carriers for their network to sell. In other words, their relationship with carriers has a big impact on what independent agents sell to their clients.

Top Intermediary Priorities

Research shows the top three reasons intermediaries place business with a specific carrier are pricing, underwriting/sales support, and compensation. While pricing and compensation are largely proprietary to each carrier, there is a lot of room to build a competitive edge through sales support.

Intermediaries are asked - what types of support carriers could provide to help drive growth. Their responses fell into three main themes:

a: Faster and easier underwriting processes;

b: Direct contact to home office personnel that can resolve issues immediately – which

b: Direct contact to home office personnel that can resolve issues immediately – which

means build a strong internal and external wholesaling program; and

c: Offering competitive and innovative products that will perform well in the long run.

These themes are echoed in other studies of experienced financial professionals. The top reason experienced financial professionals give for placing business with a carrier is because the carrier offers a strong sales process that provides a positive experience for the sales professional. Carriers that invest in making the process easier may be able to overcome slight pricing and compensation disadvantages.

Where Technology Can Help

The industry has already made significant process expanding digital services such as e-signature, e-delivery, automated underwriting, etc., streamlining the process and lowering costs. As new technologies, particularly artificial intelligence (AI), become more readily available, intermediaries are hopeful it can cut costs and improve productivity.

Research indicated 65% of intermediaries say the cost of distribution is increasing and are looking to technology to mitigate rising costs. Investments in technology span from marketing and sales enablement to data analytics, cybersecurity and compliance. Nearly 4 in 10 intermediaries agree that ChatGPT and AI will become an essential tool for BGAs and IMOs and how they do business.

This push to modernize and use technology will help address the growing U.S. life insurance need gap. Four in 10 American adults say their families would face financial hardship should the primary wage earner die unexpectedly. Making it easier and quicker for independent agents to engage today’s consumer and help them get the coverage they need is a worthy goal.

These themes are echoed in other studies of experienced financial professionals. The top reason experienced financial professionals give for placing business with a carrier is because the carrier offers a strong sales process that provides a positive experience for the sales professional. Carriers that invest in making the process easier may be able to overcome slight pricing and compensation disadvantages.

Where Technology Can Help

The industry has already made significant process expanding digital services such as e-signature, e-delivery, automated underwriting, etc., streamlining the process and lowering costs. As new technologies, particularly artificial intelligence (AI), become more readily available, intermediaries are hopeful it can cut costs and improve productivity.

Research indicated 65% of intermediaries say the cost of distribution is increasing and are looking to technology to mitigate rising costs. Investments in technology span from marketing and sales enablement to data analytics, cybersecurity and compliance. Nearly 4 in 10 intermediaries agree that ChatGPT and AI will become an essential tool for BGAs and IMOs and how they do business.

This push to modernize and use technology will help address the growing U.S. life insurance need gap. Four in 10 American adults say their families would face financial hardship should the primary wage earner die unexpectedly. Making it easier and quicker for independent agents to engage today’s consumer and help them get the coverage they need is a worthy goal.

No comments:

Post a Comment