Seeking insurance coverage in Australia, or in other parts of

Asia, is no easy task. The process typically involves the individual meeting

with a financial planner and selecting the right insurance plan. While the

process of getting insurance cover is considered a mere formality for young,

healthy individuals, it almost never is. The experience for most customers can

be frustrating.

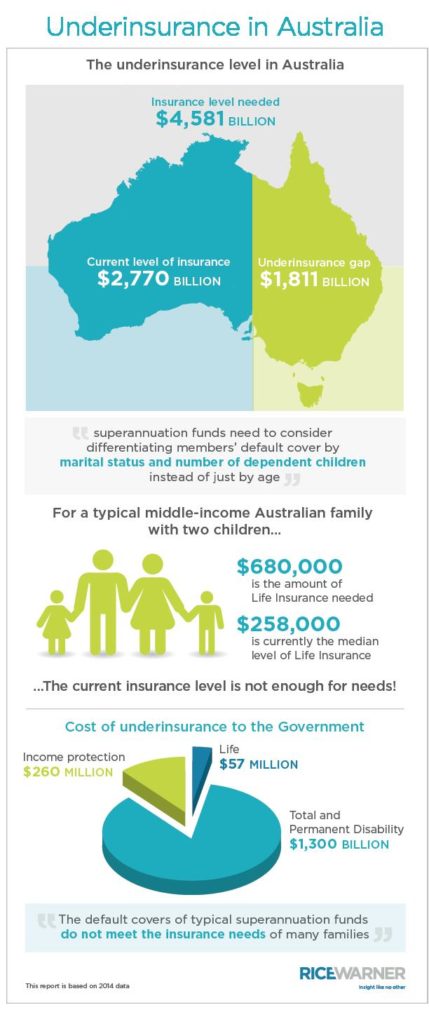

In fact, only 30-37 % of Australian between the ages of 18 and 69 have life insurance. Just

11-18 percent held disability cover, income protection insurance, or critical

illness and trauma cover. On the whole, Australia remains underinsured by A$1.8

trillion.

Individuals are required to fill out underwriting forms that are

rather cumbersome, with much of the information seemingly inconsequential. Even

if there have been past transactions with all details filled out and all

records are present with the bank or insurer, the entire process needs to be

redone. The best route is for the bank or insurer to fill out the form and for

the individual to wait to sign off.

For example, Section 10 of the form can ask for ‘Family history.’

The first question is along the lines of: “Have any of your blood related

parents, brothers or sisters (living or deceased) been diagnosed with, or

suffered from, any of the following conditions?” and it then lists

18 medical conditions followed by a nice “any other familial disorder” catchall.

How can individuals be familiar with 18 medical symptoms or conditions, even if

they are from a medical background?

Section 14 asks for “Health details” comprising over 50 questions

on various symptoms, disorders and conditions. Leaving sections incomplete adds

to delays and increases the chances of the need for medical underwriting.

This is the point at which many customers give up and storm off.

Not much has changed since the 1980s. Customers who are in greater

need of the insurance product are patient (the process could even take three

months), but those like our customer in the scenario above, who are

intentionally pursuing an insurance policy, walk out.

Why is it Cumbersome?

Several factors can illustrate why insurers are dragging their

feet over this process:

Culture–Why fix what has always worked? There is little desire to question a

process that seems to have worked for centuries. Moreover, many of the

professionals working in the industry take comfort from the degree of due

diligence done in the underwriting process. After all, more information

generally means better assessment of risk.

Business cases don’t stack up. Given the long time periods associated with paybacks from

improvements in risk selection and the potentially large spend associated with

system replacements, the business cases for taking a comprehensive review of

the underwriting process are often not as attractive as other areas with more

immediate paybacks (such as sales, claims improvement).

Complexity.

Related to the business case, this is a complex problem to solve and often

requires cooperation across multiple business lines/functions (actuarial,

finance, underwriting, advisors, distribution, technology, operations), and

coordinating a program across so many diverse stakeholders is challenging to

stand-up let alone execute, especially when many of the stakeholders don’t see

what the problem is.

How can Underwriting be Revamped?

Be clear on success metrics. Improvement in customer experience, faster decision making,

better alignment with risk appetite, and uptick in sales are typical,

high-level vision statements associated with such programs. However, it is

important that clearly measurable metrics are defined and tracked for each such

vision statement. It is also important to be clear on the prioritization among

these, as that can shift the focus of activity.

Redesign the end-to-end process rather than fixing the as-is. Far too often, underwriting

“transformation” initiatives are focused on fixing existing processes,

particularly improving the back-end, with technology seen as the main answer,

e.g., straight-through processing. While that is a useful ambition to have, it

risks only partially fixing the problem. Insurers need to start by designing

the desired end-to-end underwriting (and sales) process from a customer and

advisor’s perspective. The focus should be on minimizing hassles and improving

comfort and engagement through the process.

Harness the power of data analytics. Insurers have been investing in data analytics

for sales and pricing focused initiatives, but limited attention has been paid

to risk selection. Some considerations for insurers to think through: Which

data points are the most critical for risk selection? From the more than 100

questions being asked, how many can be removed? What alternative sources of

data can be used to better understand the customer’s risk profiles?

Automate ruthlessly. Leading insurers globally have been testing the use of

Robotic Process Automation (RPA) to automate processes across the value chain.

There is a significant opportunity for insurers to cast a critical eye on all

repetitive and manual elements in the underwriting decision-making process, and

to start exploring how these elements can be automated. Pre-populating forms

with existing information (from banking partners and other data sources),

further automation of the rules-based decisions, and the processing/fulfillment

at the back-end should be three areas of immediate focus.

Set up the right team. Typical project teams of project managers and business

analysts are helpful, but they need to be supplemented with critical skill

sets. Examples of the types of roles that many insurers are including in such

programs include but are not be limited to: UX/UI designers for rapidly

developing the desired customer experience, technical designers for rapid

prototyping, behavioral psychologists for testing customer response to how

questions are asked, and SMEs from other industries to inject fresh

perspectives and continue innovating.

Implement in an agile manner. References to the agile work process have irked me in the

past but having recently migrated from doing multiple agile courses to actually

launching a product from concept to in-market in 14 weeks, I have become a true

believer in this approach to project management over the traditional

waterfall-based approach still dominant at most organizations. Given the

cross-functional span of underwriting, it is important to rapidly test new

concepts with customers (such as shorter forms, different questions, willingness

to divulge new information) and advisors and incorporate learnings in

redesigning the future state process.

Look outside the industry for inspiration. Given the slow pace of change in the life

insurance industry, it is helpful to look at how underwriting processes are

changing in others. The mortgage industry has many parallels to the life

insurance industry: largely intermediated businesses and an overly complex

underwriting process. Players such as

Quicken Loans have rewritten the rule books by recently launching

an online mortgage where customers can get full approval in as little as eight

minutes. Similar changes are appearing in SME lending, where a number of

fintechs and incumbents have redesigned their underwriting processes using

better data, advanced analytics and customer-centric interfaces to not only

improve existing customers’ experiences, but also to tap into underserved

segments that had been turned down by banks using traditional methods.

Risk selection lies at the core of an insurance business’s

operations. Insurers have the opportunity to not only fundamentally enhance

this process but also realize material cost savings and deliver a superior

experience to customers and advisors. Redesigning an underwriting process is

not a straightforward task, but given the large size of the

opportunity and increasing amounts of venture capital flowing into insurtechs,

incumbents need to act now.

No comments:

Post a Comment